Your Ride: Vehicle Factors

Fortunately, vehicle-related factors are often within your control. In this section, we’ll break down how your ride can raise or lower your auto insurance rates — and what to consider when buying or insuring a car.

Make & Model

It’s no surprise that a flashy sports car costs more to insure than a modest sedan. Insurers consider your vehicle’s body type, performance features, safety record, and even theft rate when determining your premium.

Top 5 Safe Cars That Could Lower Your Insurance Premium

Choosing a car with top-tier safety ratings can make a real difference in your insurance cost. Here are five highly rated vehicles that are known for their safety features and affordable insurance premiums:

| Vehicle | Why It’s Insurance-Friendly |

|---|---|

| Subaru Outback | Excellent crash ratings, standard all-wheel drive, and EyeSight® driver assist |

| Honda CR-V | Strong safety scores and reputation for reliability and low repair costs |

| Toyota Camry | Top IIHS safety ratings and widely available affordable replacement parts |

| Mazda CX-5 | Standard safety tech and strong crash protection without luxury pricing |

| Hyundai Tucson | High safety scores and a lower theft rate compared to similar SUVs |

While insurance rates depend on many factors, driving one of these safe and practical vehicles could help reduce your premium, especially if paired with a clean driving record and low annual mileage.

- High-performance cars like sports coupes or turbocharged models are often driven faster and more aggressively, which increases accident risk — and premiums.

- Luxury vehicles have expensive parts and labor, making them pricier to repair or replace after a loss.

- Family-friendly vehicles like minivans and midsize SUVs tend to have lower accident involvement and strong safety records, which helps lower premiums.

- Frequently stolen models (even older cars) may carry a surcharge depending on your location.

If you’re shopping for a car and want to keep your insurance costs down, prioritize models with strong safety ratings and a low cost of ownership. Many insurers offer discounts for vehicles equipped with like automatic emergency braking or lane departure warnings.

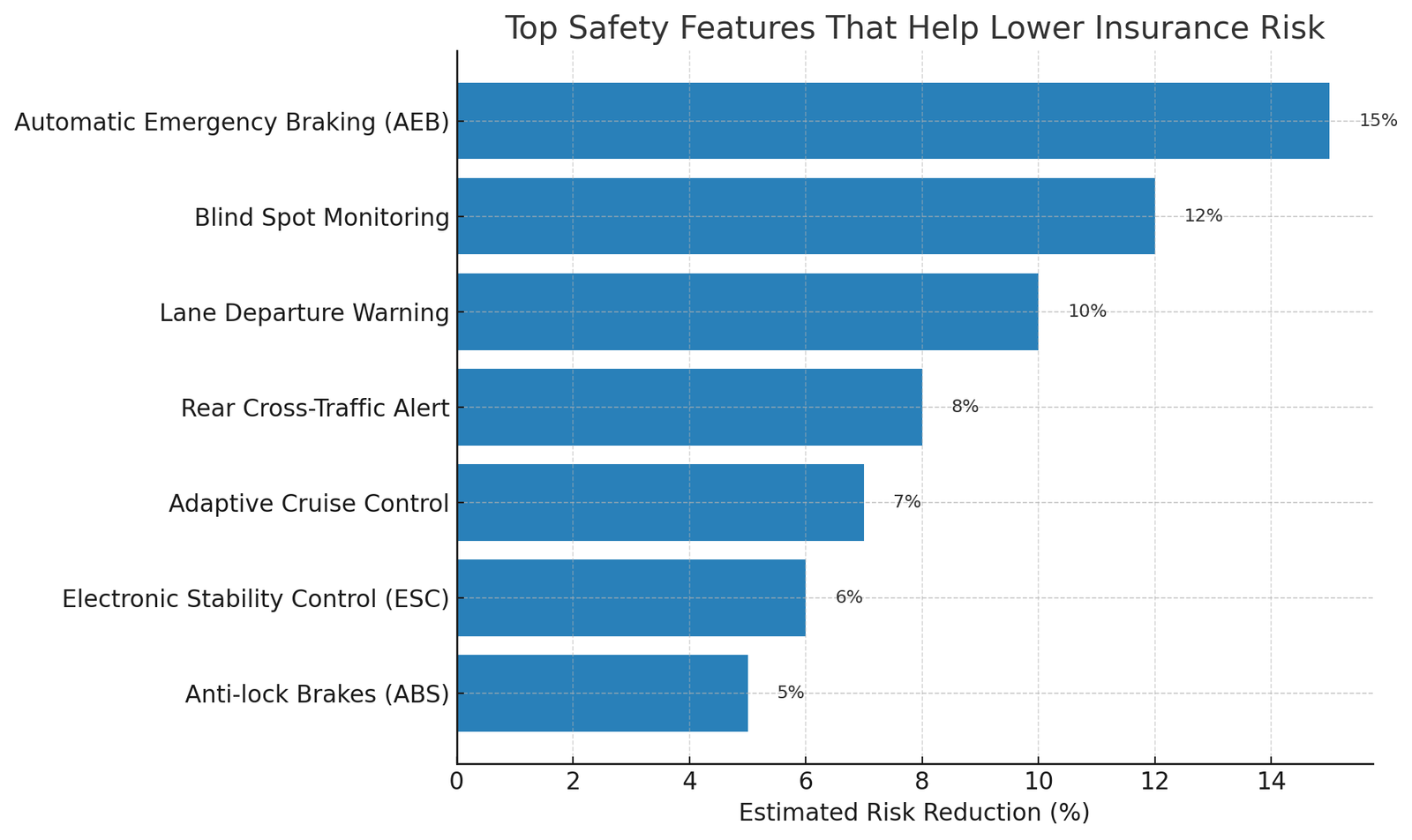

Top Safety Features That Help Lower Insurance Risk

Cars equipped with advanced safety features are statistically less likely to be involved in serious crashes — and that can lead to lower insurance premiums. Here’s a quick look at some of the most impactful technologies:

Features like Automatic Emergency Braking (AEB), Blind Spot Monitoring, and Lane Departure Warning systems are often factored into your rate — especially for newer vehicles. The more your car helps you avoid accidents, the less risk the insurer has to cover.

Vehicle Value

The more your car is worth, the more it costs to insure — especially if you carry comprehensive and collision coverage. These optional coverages pay to repair or replace your car if it’s damaged in an accident, stolen, vandalized, or hit by weather-related events.

Insurers base their payouts on the actual cash value (ACV) of your car at the time of loss. A brand-new car with a high sticker price means a potentially larger payout, so your premiums will reflect that risk.

Here’s how vehicle value typically affects rates:

| Vehicle Type | Impact on Premium |

|---|---|

| New luxury SUV | High — due to expensive parts and high ACV |

| Used midsize sedan | Lower — lower replacement cost |

| Classic or collectible car | Variable — may require specialized insurance |

Keep in mind: if your car is financed or leased, your lender will usually require full coverage until the loan is paid off. That means you may be paying a higher premium simply due to the vehicle’s value — whether or not you drive it frequently.

How Much You Drive

Annual mileage is a significant risk factor. The more time you spend on the road, the greater your chance of being involved in an accident — and insurance companies price your policy accordingly.

Insurers typically ask for an estimate of how many miles you drive each year. If your mileage is well below average (usually under 7,500 miles/year), you may qualify for a low-mileage discount. On the other hand, long commutes or high-usage vehicles often come with rate increases.

Let’s break down how this works:

- Under 7,500 miles/year: May qualify for low-mileage discounts

- 7,500–15,000 miles/year: Considered average usage

- 15,000+ miles/year: May trigger higher premiums

Some companies also offer usage-based insurance (UBI), which tracks how much — and how safely — you drive through a mobile app or plug-in device. If you’re a low-mileage driver, this could be a cost-saving option. You can learn more about this on our Driving Behavior page.

Final Thoughts

Vehicle factors may seem straightforward, but they have a significant impact on your insurance rate. The good news? Unlike some other rating factors, your choice of vehicle is something you can control.

By driving a safe, reliable car and minimizing your annual mileage, you can keep premiums manageable — even if other factors are working against you.

Interested in what else affects your premium? Check out: