GAP Car Insurance Explained

Gap insurance (Guaranteed Asset Protection) is optional auto insurance coverage that helps pay the difference between your car’s actual cash value and the remaining loan or lease balance if your vehicle is totaled or stolen. Without it, you may be left paying for a car you no longer have.

Why Do You Need Gap Insurance for a Car Loan or Lease?

New and leased cars depreciate rapidly—often losing 20% or more of their value in the first year. If your vehicle is declared a total loss after an accident or theft, your standard auto insurance policy typically only covers the vehicle’s market value. Gap insurance coverage helps cover the financial “gap” between what your insurer pays and what you still owe.

Many auto industry professionals have seen firsthand how gap insurance protects car buyers from serious financial losses. When a vehicle is totaled, this coverage can pay off the remaining loan or lease balance, saving you from debt on a car you no longer own. It’s one of the most valuable protections for leased or financed vehicles.

Real Story from the Car Sales Floor

I was in car sales and sold a car to a couple who traded in a vehicle with severe negative equity. They owed much more on their old car than it was worth, and that debt was rolled into the new loan.

They ended up financing $43,000 on a new car with an MSRP of $34,700. Just three months later, the vehicle was totaled in an accident. Their insurance company paid out $30,000 for the car — far less than what they owed.

Fortunately, they had GAP insurance. It covered the remaining balance of their loan, saving them from thousands in unexpected debt.

GAP insurance is definitely worth it — especially if you’re financing close to or above MSRP.

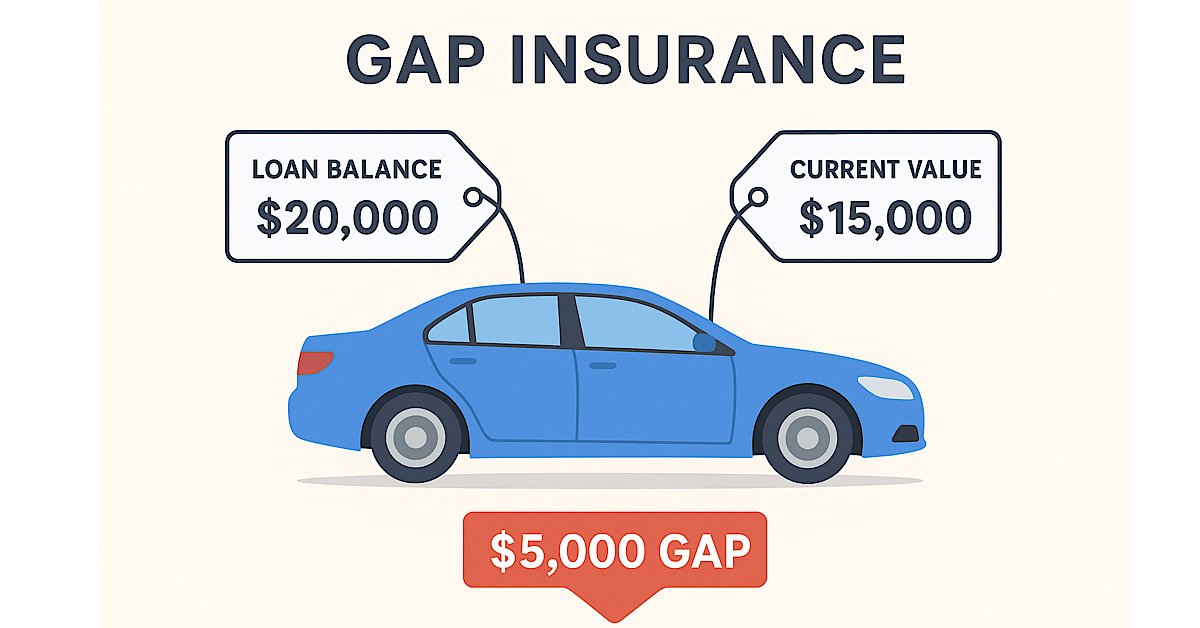

How Does Gap Insurance Work?

Here’s how gap insurance works: If your car is totaled or stolen and your insurance payout is less than your remaining loan or lease balance, gap coverage pays the difference. For example, if you owe $20,000 on your loan but your insurance only pays $15,000, gap insurance covers the remaining $5,000.

Who Should Consider Buying Gap Insurance?

- Drivers who lease or finance their vehicles

- Owners of new cars that depreciate quickly

- Anyone whose loan or lease balance is higher than their vehicle’s current value

What Does Gap Insurance Not Cover?

Gap insurance only covers the difference between your auto loan or lease balance and your car’s actual value. It does not cover:

- Your insurance deductible

- Damage repairs if the car is not declared a total loss

- Personal property inside the vehicle

- Extended warranties or loan rollover from previous vehicles

Is Gap Insurance Required?

Gap insurance is usually optional, but some lenders or leasing companies may require it until your balance drops below the car’s market value. You can buy gap coverage from your auto insurer, car dealership, or a third-party provider.

How to Get Gap Insurance

There are several ways to purchase gap insurance:

- From your car insurance provider as an add-on

- Directly from the dealership at the time of purchase or lease

- Through specialized gap insurance providers online

Compare rates and options carefully. Dealership-provided gap insurance is often more expensive than adding it to your existing car insurance policy.

Benefits of Gap Insurance

- Protects you from paying out-of-pocket on a totaled or stolen car

- Gives peace of mind when financing or leasing a vehicle

- Helps avoid negative equity after a total loss

Frequently Asked Questions About Gap Insurance

Is gap insurance worth it?

Yes, gap insurance is often worth it if you’re financing or leasing a car, especially a new one. It provides crucial financial protection if your car is totaled and you still owe more than it’s worth.

How much does gap insurance cost?

Gap insurance typically costs $20 to $40 per year when added to your existing car insurance policy. Buying it from a dealership can be more expensive, often bundled into your loan.

Can I cancel gap insurance?

Yes, most providers allow you to cancel gap insurance once your car’s market value exceeds your loan or lease balance. Check with your insurer or lender for cancellation policies.

Does gap insurance cover theft?

Yes. If your car is stolen and not recovered, gap insurance will pay the difference between your auto insurance payout and what you still owe on the vehicle.

Is gap insurance included in full coverage?

No. Gap insurance is a separate add-on. Full coverage usually refers to liability, collision, and comprehensive insurance.